After the peak on December 16, Nasdak – Who traces almost all stock trading on the Nasdak Stock Exchange- entered into a correction. The index has decreased about 9 % years so far and 13 % of the December summit.

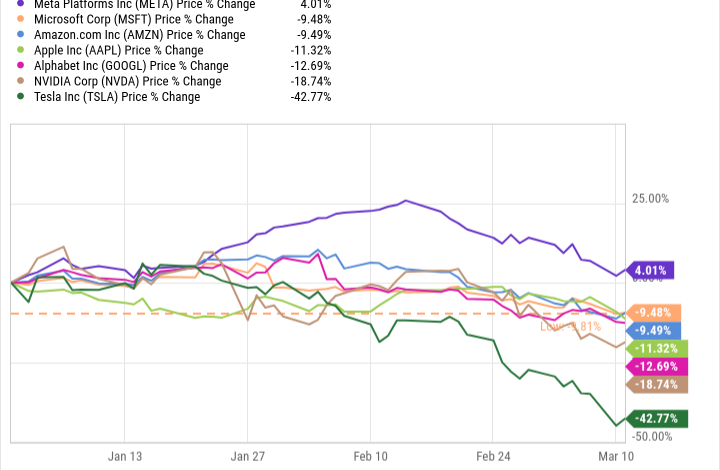

Given that Nasdaq Composite is heavy technology, it is not surprising that many large -names technology shares have followed a similar path this year. “Seven Wonderful”, which is given apple (Nasdaq: Aapl)and Microsoft (Nasdaq: msft)and Nafidia (Nasdaq: nvda)and Amazon (Nasdaq: amzn)and Definition platforms (Nasdaq: Meta)and alphabet (Nasdaq: Goog(Nasdaq: Googl)And Timing (Nasdaq: tsla)All have decreased a year so far, except for the definition.

Meta data by ycharts.

I don’t see a decrease in the wonderful seven stocks as time to press the panic button. They have suffered from both similar retreats before, and with enough time, they would likely test them again at some point. If there is anything, I consider this time for investors to think about shopping “discount” and start buying shares on a decrease.

I see the call almost every seven and I will think about buying a decrease on each of them. However, the only exception is Tesla Stock, in which I will personally stay away from now.

For the remaining six shares in the wonderful seven, there are growth drivers and competitive advantages in their business that make the purchase of the decline attractive:

Apple is one of the most profitable companies in the world and has an increased service sector that expands quickly to the iPhone and other devices.

Microsoft has a broad -technology ecological system for institutions and corporate life as we know, and a strategic partnership with Openai gives it a leg in creating artificial intelligence.

NVIDIA graphics units (GPU) and other data center devices are vital to the development of Amnesty International’s infrastructure that will be developed for the foreseeable future.

Amazon has advanced beyond e -commerce to become a leader in cloud computing and has emerging advertising works.

Meta is a digital advertising giant, and has invested extensively in the infrastructure of Amnesty International to support its business and present its descriptive vision in life.

Google from Alphabet continues to control the search, and its cloud work continues to pick up Steam, and YouTube continues to be the pioneer in digital video content and emerging broadcasting power.

Of course, these are simplified business analyzes, but I am more optimistic about each of its paths than Tesla.

Electric cars for passengers (EVS) represent most of Tesla revenues, and many of these sales come internationally. Unfortunately, Tesla sales abroad recently achieved great success. China, Norway, Denmark, Sweden and Germany are marketing all experienced sales declines in recent months.

Not only the EV market becomes more competitive with the international companies that launch their EVS (such as Byd In China and Volkswagen In Germany), but many of them are also cheaper. With the same performance in most cases, it is not surprising that customers tend to a cheaper option.

Car revenues in Tesla in the fourth quarter of 2024 amounted to $ 19.8 billion (a decrease of 8 % on an annual basis), while its total revenue increased by 2 % on an annual basis to $ 25.7 billion. Certainly, investors expect more Tesla revenues, but its 23 % decreased income in its income was more concerned, as it continued its inhibitory path during the past few years.

TLA revenue data (quarterly) by Ycharts.

Even after it decreases by more than 42 % this year, Tesla remains expensive in most criteria. Looking at the percentage of its price to profits (P/E), it is definitely the most expensive of seven wonderful-not soon.

The percentage of tsla PE (annual) by Ycharts.

It will be difficult to justify investment in Tesla while this is expensive and its profits growth have stopped. It seems that the other seven wonderful stocks have greater growth in the profits in front of them, and there are less questions about the future of their business.

When you invest in Tesla, you invest in a vision (which is not bad by its nature), but you should give up caution when there are a lot of question marks and arrows expensive.

Have you ever felt that you missed the boat in buying the most successful stocks? Then you will want to hear this.

On rare occasions, our expert team issues an analyst A. “Double Permanent” stock A recommendation for companies they believe is about to pop. If you are worried that you have already missed your chance to invest, it is now the best time to buy before it is too late. And the numbers speak for themselves:

Nafidia:If you invest $ 1,000 when we doubled in 2009,You will have 282,016 dollars!

apple: If you invest $ 1,000 when we doubled in 2008, You will have $ 41,869!

Netflix: If you invest $ 1,000 when we doubled in 2004, You will have $ 482,720!

Currently, we make “Double Download” alerts for three incredible companies, and there may not be another chance like this any time soon.

He continues.

*The stock consultant dates back from March 10, 2025

John Maki, former Chole Foods Market, a affiliate company, a member of the Motley Fool Board of Directors. Randy Zuckerberg, former Director of Market Development and Speak for Facebook and Sister to Meta Platforms, Mark Zuckerberg, member of Motley Fool Board of Directors. Susan Fry, CEO of Alphabet, is a member of the Motley Fool Board of Directors. Stefon Walters has sites in Apple and Microsoft. Motley Fool has positions in Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. Motley Fool Company byd and Volkswagen AG recommends the following options: Long from January 2026 $ 395 calls on Microsoft and Short January 2026 $ 405 calls on Microsoft. Motley Fool has a disclosure policy.

Nasdak Correction: I will think about buying “amazing seven” shares – except for this one was originally published by Motley Fool