Pepsico(NASDAQ: PEP) It was a fruitful investment for generations. The company earns enough money to exchange profits with investors through profits and raise the amount it pays for 52 consecutive years. You can call it a range of products for selling loved foods and drinks to a global customer base of about 8.2 billion people (and grow). There is just an endless runway to grow.

However, arrows in stagnation. Pepsico has decreased by 25 % since its rise in 2023. It is a rare decrease for a respectable company, and it has decreased since the financial crisis in 2007-2009. Should investors buy Pepsico in 2025, or is the company its climax?

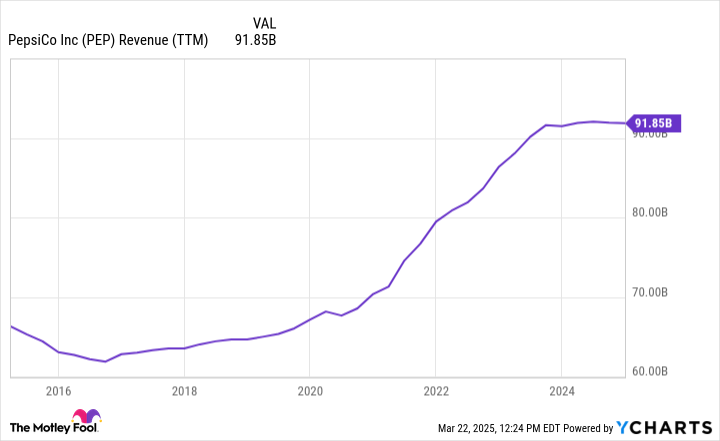

Pepsico has grown for decades by selling more products, launching and gaining new brands, and raising their prices. However, growth has increased on prices since the Covid-19s. At the nominal value, the graph below shows that the works have been great, with impressive growth over the past five years.

Pep (TTM) revenue data by ycharts

However, it is not the entire story. According to the data of the Federal Reserve in St. Louis, the price of 16 ounces of potato chips in the United States has increased by 44 % since January 2020. The typical soda bottle is increased by the brand data, but Pepsico is the largest snack company and the second largest non -alcoholic beverage company in the United States, you can deliver points here reasonably.

It is not that Pepsico tied his pockets. Its total margin is almost the same today five years ago. Instead, it reflects growth through inflation rather than buying consumers more. The problem is that consumers will not tolerate the high prices for a long time. Pepsico achieved 2 % growth in 2024, but their sizes decreased by 1 %, so they were all driven by the price. Freito Lay sizes fell by 2.5 % in North America, and drinks decreased by 3 %.

Consumers seem to be tired of high prices. At least in the short term, it may cost it to increase the number of prices in prices, which compensates for the benefit from raising prices. I do not say that Pepsico will not grow, but the company can struggle to move the needle after the past five years.

Don’t worry. Pepsico does not face collapse. This is still a reliable work and investors can hope.

Most people buy Pepsico shares to distribute profits. The company owns profits, and it is unlikely to change any time soon. The profit distribution percentage is about 65 % of profit estimates 2025. The castle -like budget in Pepsico is a nice safety network, with a comfortable $ 9.2 billion in cash and credit classification in the investment area.

Pepsico prices may lead to some shoppers, but it is difficult to imagine a significant decrease. The company’s brands are home favorites and include products such as Pepsi, Mountain Dew, Gatorade, Doritos, Lay’s, Cheetos, Crufles, Crush and Quker, among many. Pepsico sales of 12 months have not decreased more than 7.6 % in 15 years.

Again, growth may slow down, but investors may still expect modest growth and additional profit distributions.

As wonderful like Pepsico, investors should be very vigilant over the evaluation. Over payment of slow growth arrow can be catastrophic on the total investment revenues.

Pepsico shares mainly slip because the market adapts to low growth expectations. The price rate to the profits of Pepsico and the long -term growth estimates decreased to its lowest levels:

PEP PE ratio by ycharts

The good news is that the profit return has risen to 3.7 %, which is the highest level ever. High profit returns are often a red mark, but not in this case. Investors get more urgent profit income for their money because the market expects a decrease in growth (estimation of the share price).

So, does Pepsico buy?

From the point of view of pure growth, profits are approximately 21 times are an expensive evaluation of 4 % annual growth to 5 %. However, investors are repeatedly pushing blue chips like Pepsico because they can be relied upon. You can reasonably assume that Pepsico will remain here decades from now.

It is difficult to name Pepsico with a strong purchase without more growth capabilities. The profit investors can argue over the high and reliable return, but otherwise, I think the arrow will be more attractive at P/E closer to 15 to 17.

Have you ever felt that you missed the boat in buying the most successful stocks? Then you will want to hear this.

On rare occasions, our expert team issues an analyst A. “Double Permanent” stock A recommendation for companies they believe is about to pop. If you are worried that you have already missed your chance to invest, it is now the best time to buy before it is too late. And the numbers speak for themselves:

Nafidia:If you invest $ 1,000 when we doubled in 2009,You will have $ 305,226!

apple: If you invest $ 1,000 when we doubled in 2008, You will have $ 41382!

Netflix: If you invest $ 1,000 when we doubled in 2004, You will have 517,876 dollars!

Currently, we make “Double Download” alerts for three incredible companies, and there may not be another chance like this any time soon.

He continues.

*The stock consultant dates back from March 24, 2025

Justin Bob has no position in any of the mentioned shares. There is no position in Motley Fool in any of the mentioned stocks. Motley Fool has a disclosure policy.

Is Pepsico to buy, sell or contract in 2025? It was originally published by Motley Fool