Natural Gas Dominance Unchallenged in Global Energy Landscape.png

With a lot of the world’s attention focus on wind turbines, solar panels and electric cars, natural gas grew on the importance of the spine of modern energy systems. It nourishes power stations, high temperatures, disk engines, and – through LNG (LNG) – Confederations. The newly released statistical review highlights the 2025 global energy how it has become indispensable, despite the escalating pressure on the removal of carbon.

By following the previous article on the trends of production and global consumption of production and consumption, let’s move in the numbers behind the global gas market, with a focus on production, consumption and the increasing importance of liquefied natural gas exports.

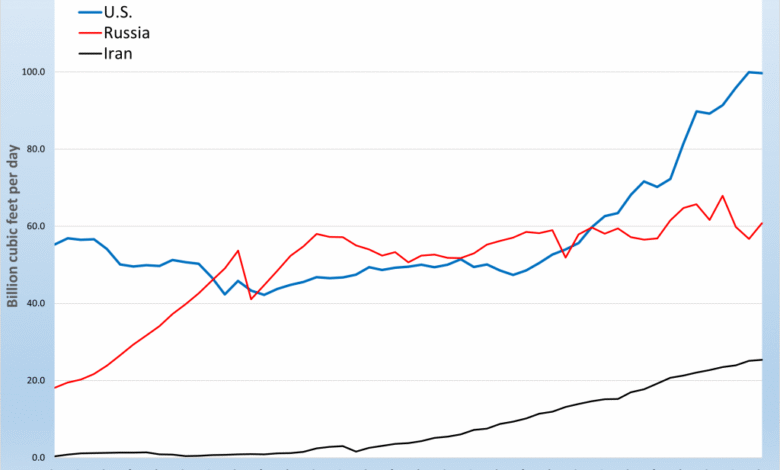

In 2024, global natural gas production reached 398.0 billion cubic feet per day (BCF/D). The United States alone made up 25 % of it, producing less than 100 BC/d. This was a slight decrease in the repermal output in 2023, but it is still more than five times the production of Canada, its closest counterpart in North America. Many of this force comes from the rock gas revolution that started about 20 years ago, transforming the United States into the largest natural gas producer in the world and ultimately the liquefied natural gas source in the world.

Russia, which the United States exceeded for the first position among gas producers in 2011, is still the second largest producer in the world, with 60.8 BCF/D from production in 2024. But this number remains less. Moscow has tried to the Asian market axis, but logistical and political obstacles slowed progress.

Among the other major producers:

Iran and QatarWhich are still vital players in the Middle East, as it produces about 25 and 17 BCF/D, respectively.

ChinaAnd, which has doubled the production of home gas over the past decade, is now 23 BC/D-which is an impressive achievement as the country pushes the displacement of coal with burning alternatives.

AustraliaAt 14 BCF/D, she played a global leading role in LNG, although future growth may be restricted through aging fields and organizational pressure.

Africa’s contributions are modest in comparison. Algeria leads the continent with 9.1 BCF/D, followed by Egypt and Nigeria. Breaked infrastructure and harsh investment have limited the capabilities of the broader continent.

It is worth noting that during the past decade, more than half of the growth of global natural gas production came from the countries of the Organization for Economic Cooperation and Development, although production in the European Union has decreased by two thirds. This confirms that despite the global payment towards renewable energy sources, countries are still seeking to obtain flexible energy supplies that balance the ability to withstand costs with a decrease in carbon density.

The global consumption of natural gas in 2024 was the highest level ever reached 398 BC, more than twice the level that was seen in 1990. A lot of this growth was motivated by the countries not affiliated with OECD-especially Asia.

The United States is still the largest consumer in the world in 87 BC/day, representing about 22 % of global demand in 2024. Russia ranked second in 46 BC/day, despite slowing growth over the past decade.

Third place, with more than twice the past ten years to reach 42 BC/d. This reflects both rapid manufacturing and government efforts to reduce air pollution by transforming growth away from coal.

It includes other prominent consumers:

Iran: 24 BCF/D, to a large extent for home use.

Canada and Kingdom of Saudi ArabiaAbout 12 BCF/D each, to a large extent for petrochemicals and power.

Japan and Germany: Less than 9 BCF/D each, with both signs of a decrease with efficiency measures and the acquisition of renewable energy sources.

India: 6.8 BCF/D, grows gradually, especially in the fertilizer and energy sectors.

At the regional level, Asia and the Pacific Asia in North America caught almost in consumption. As of 2024, the region represents 23.6 % of global demand – led by China, India and Japan. The Economic Cooperation and Development Organization countries still constitute more than 43 % of the total, but there has been no total growth since 2018.

Even Africa, a minor for gas demand, began to expand. Countries like Algeria and Egypt are witnessing stronger growth, due to improving energy access and local gas resources.

Data tells a convincing story: Over the past decade, 74 % of the growth growth of global demand from 70 BC came from non-central countries-a reflection since the early first decade of the twentieth century when he led the developed world expanding.

If there is one slice that turned global gas dynamics in the past decade, it is a liquefied natural gas. In 2024, LNG’s global exports reached about 546 billion cubic meters – or nearly 53 BCF/D – since 2010.

The United States is now leading the world in liquefied natural gas exports, charging more than 11 BC in 2024. Just 15 years ago, the United States was building liquefied natural gas import plants. Today, it is not only the self -sufficiency of energy, but also helps the allies diversify away from the Russian offer.

Qatar, the world leader for a long time, ranked second after 10.3 barrels per day. Although export volumes have fallen, Qatar is largely investing in capacity expansion and can regain its crown in the coming years. Australia is close, also at 10.3 BCF/D, but it faces low production of mature fields.

Among the other prominent exporters:

Russia: 4.3 BCF/D LNG exports – which have been identified through penalties and the development of slow infrastructure.

Nigeria and AlgeriaThe backbone of Africa with 4.9 BCF/D from liquefied natural gas exports between them.

Malaysiaand IndonesiaAnd BruneiImportant suppliers in the Asia Pacific region, although new arrivals.

Papua New Guinea: Rising player, with more than 1.1 BCF/D in LNG exports despite the market recently entered.

Trinidad and Tobago: The main resource of liquefied natural gas in the Caribbean Sea region, despite its low production of the previous highlands.

Europe mostly remains a consumer of liquefied natural gas instead of supplier. Norway contributes modestly, while the rest of the continent plays a marginal role in exports.

Perhaps the most important note here is how liquefied natural gas trade has shifted from a few of the main producers into a wide mix of suppliers across five continents. This diversification created a more liquid and flexible gas market.

Despite extensive climatic obligations, natural gas is still necessary for global energy stability. Its role has not been growed as a bridge fuel – responding to coal while enabling the growth of discovered renewable energy sources – only in recent years.

However, the challenges remain. Prices, infrastructure restrictions, and increased organizational pressure – especially in Europe – are reshaping how gas is produced, transported and consumed. The organizational pressure will continue to capture carbon, mixing hydrogen, and lower methane emissions in the development of the scene.

But if the past decade is any evidence, then natural gas is far from being outdated. It is universal, flexible and adaptable – and if there is anything, it has strengthened itself as a calm giant in the energy world.

Written by Robert Rapier

More readings from OilPrice.com:

Read this article on OilPrice.com

Don’t miss more hot News like this! Click here to discover the latest in Business news!