Why Costco Stock COST May Be a Smarter Investment Than.jpeg

Costco has always been a favorite on the market, but its current evaluation contains the most upscale investors who raise eyebrows as the company trades near its highest levels ever. trading in profit complications that exceed some of the world’s largest technology giants, it is fair to ask: How can a warehouse selling toilet paper and grill chicken may justify this sharp bonus? At first glance, do not add numbers. COSTCO comparison to technology companies indicates a fairly enlarged evaluation in favor of a wholesaler.

Costco comparison results (cost)

Shy growth expectations, delicate margins, and the business model that has not changed much for decades not completely shouting. However, Costco continues to climb – in my opinion, in my opinion, due to one major factor: perceive the risk. Since the company’s business model is largely established in the frequent repeated revenues of the membership fee, its profit is exceptionally stable.

It can be said that this stability justifies the noble evaluation of the stock – and the backbone of my upscale thesis is, even if there is no significant safety margin.

I agree with Costco’s critics – those who are skeptical in a warehouse full of various commodities that are traded in P/E forward from 58, which is literally multiple than the technology giant and AI Trailblazer Nvidia. For a company like Costco, which has grown revenue at an annual compound rate of 10 % over the past five years and operating 15 % – analysts are only expected for analysts to grow revenue at an annual growth rate over the next five – it is in reality, at first glance, so that the company can trade in such severe installments.

Costco (cost) revenues, profits and profit margin

But here is what many market participants miss when analyzing companies: the evaluation based on net profit is largely based on one major factor. Unlike profits, there is no single scale universally acceptable to risk. Some investors focus on the experimental version, while others consider organizational threats or exposure to a macroeconomic. In the end, each investor looks at the situation through his own lens.

This is the place that highlights Costco as a rare case: a frequent revenue model outside the technology sector. Customers pay annual organic fees – ranging from $ 60 to $ 120 in the United States – only to shop in their warehouses. Costco is likely to convert all of this directly to operating profits (although the company does not explicitly reveal it), allowing the company to be very profitable even while selling goods on shaving margins.

In the last quarter, the membership income increased by 10 % on an annual basis, with a 93 % amazing renovation rate in North America. This type of brand loyalty and engraved value creates a business model with a very small risk of profit fluctuations. For this reason, Costco works like defensive inventory, which provides low risks and a high degree of ability to predict returns. Therefore, while the evaluation may appear on the surface, this level of stability and cash flow justifies what justifies the complications of installments.

While only about 2 % of the total COSTCO revenue comes from membership fees, these fees represent more than half of the total operating income of the company. On this type of size, there is no other retail seller that can withdraw a large -sized -sized -size model just like the warehouse giant in ISSAQUAH, based in Washington. The main street data indicates that Costco’s revenues rise while organic fees remain an essential component.

Costco revenues (cost) according to the sector

For this reason, even during periods of weakness for consumer spending, Costco tends to remain very profitable – not only because of its membership model, but because it constantly acquires the market share of competitors. By maintaining the fine margins on the estimated elements, and with shoppers naturally turning towards the basics during the times of financial stress, Costco puts pressure on competing retailers who cannot simply match their prices without cutting their own profit.

Take Q3, for example: Costco sales increased by 8 % year on an annual basis to $ 62 billion, while their peers like TGT (TGT) has seen the contraction of similar sales and was forced to review profit instructions down. This highlights how Costco is not just the opposite wind of the macroeconomic – it is actually growing through it. In other words, the macro risk appears to have a much lighter effect on a company like Costco.

Costco (cost) compared to Walmart and Target

Although the relatively low -risk business model may require evaluation premium, it is useful to explore what the appropriate stock price may appear in light of simplified assumptions.

For this analysis, I will appreciate the value of Costco’s shares using the main addiction -based cash flow model. Let’s start with the fact that in the 2024 fiscal year, Costco achieved about $ 4.8 billion of membership fee revenues. Although this is not equivalent to a free cash flow, it is a reasonable agent to repeat the operating cash flow due to its stable and high -sideline nature.

With the current market value of Costco at about $ 470 billion, we can manufacture the evaluation. If we assume a 6 % discount rate-as it is reflected on the lateral appearance of relatively low risk although the treasury return for 10 years sit about 4.4 %-and a permanent growth rate of 5 %, the value of the implicit shares is about 480 billion dollars, or about 1083 dollars per share. This is closely compatible with the current Costco share price.

Costco (cost) the date of shares from year to date

These assumptions seem somewhat reasonable and indicate that Costco’s evaluation has what justifies it under optimistic circumstances, but they are not unrealistic. However, the use of a 7 % discount rate is more conservative, while maintaining other constant assumptions, would significantly reduce the value of implicit stocks, almost half.

In short, although Costco does not show an exaggerated value in light of favorable scenarios, the current evaluation leaves a big area of error. A margin of meaningful safety may not appear unless the macroeconomic conditions, such as stagnation, may turn to a decrease in risk -free rates, and therefore, greater tolerance of high evaluation complications.

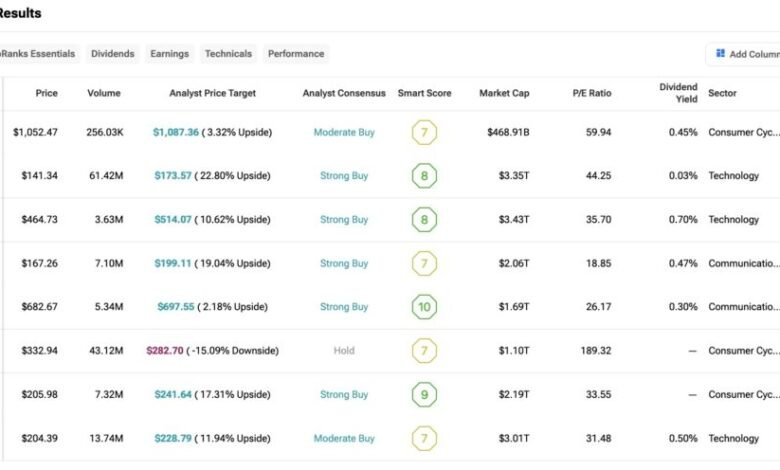

Of the 25 analysts who have covered the cost in the past three months, 17 assessed the shares as a purchase, while the remaining eight calls them. Therefore, although the overall feelings are moderately difficult, the average target price of $ 1,096.36 means ~ 8.5 % of the current share price over the next twelve months.

See more cost analyst assessments

Due to the strength and stability of the Costco’s basic business model, the excellent assessment complications appear justified. Nowadays, there are no big concerns that will challenge the constructive view of the stock. However, it is important to note that the current evaluation provides limited – on anything – safety.

As such, keep careful He buys Category on Costco. Although the upward trend in the near -term may be restricted, the company remains in a good position to provide a long and long -term growth.

Eliminate responsibility and disclosure is an issue

Don’t miss more hot News like this! Click here to discover the latest in Business news!